Good morning,

Welcome to the best way to stay up-to-date on India’s financial markets. Today, we share with you takeaways from Dr. Viral Acharya’s remarks at our live event on Wednesday.

Have a question you want us to answer? Fill out this form and you could be featured in our newsletter.

—Shreyas, [email protected]

Market Update.

Takeaways from Dr. Viral Acharya's Remarks

On Wednesday night, at Samosa Capital’s inaugural live event, Dr. Viral Acharya spoke to an audience of around 70 professionals in New York, addressing key questions about India's economic future. His presentation centered on two main inquiries: Is India's macroeconomic stability a temporary phenomenon or a sustainable trend? And, is India experiencing a "savings glut of the rich" that distorts the broader economy? These questions served as a springboard for further discussion on institutional reforms, structural issues, and policy recommendations.

Reforms

Since the Global Financial Crisis, India has introduced significant reforms to its monetary and banking systems. One key development was the introduction of inflation targeting in 2013, with a goal of 4 percent inflation (within a ±2 percent band). The formation of the Monetary Policy Committee (MPC) in 2016 further institutionalized India's approach to monetary policy. These reforms have moved India toward a more rule-based system, similar to the European Central Bank, Federal Reserve, and Bank of Japan, in contrast to the discretionary policies India had employed in the past.

In addition to these monetary reforms, India has seen a marked improvement in economic data, thanks to the external benchmarking of loans to improve monetary transmission. This innovation has made interest rate decisions more effective in reaching borrowers. Furthermore, the Reserve Bank of India (RBI) has gained greater independence and credibility, which has allowed it to shape economic outcomes with greater precision.

India's banking sector has undergone its own transformation, especially after the non-performing asset (NPA) crisis of 2015–2018. During this period, bad loans grew to unsustainable levels, but several reforms have helped rectify the situation. For instance, asset quality reviews have enabled better stress testing of banks, and the NPA resolution framework has provided mechanisms for debt restructuring and refinancing. Bank recapitalization was a crucial step in infusing liquidity into public sector banks, which has helped to stabilize lending and foster stronger credit flow.

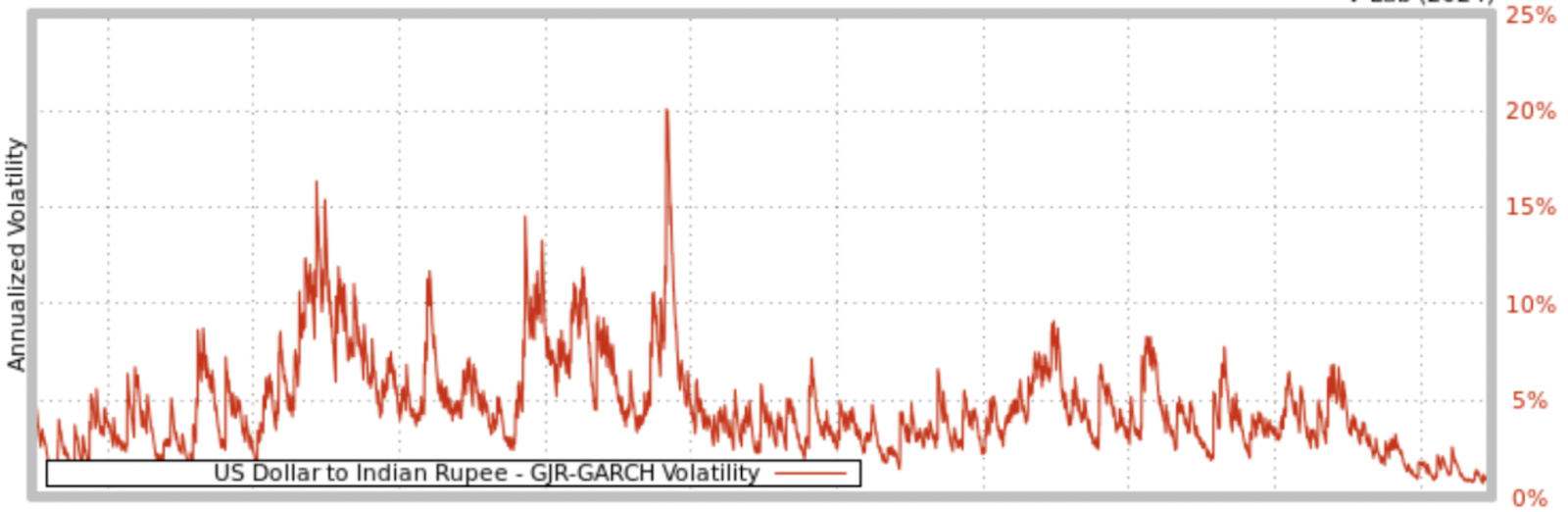

In terms of market operations, the RBI has also enhanced its management of foreign exchange reserves, reaching a peak in late 2024. This has played a significant role in reducing currency volatility and mitigating the risks of sudden capital flight. On the government side, the introduction of the Goods and Services Tax (GST) and a shift towards capital expenditure (CapEx) have helped boost infrastructure, contributing to improved exports and economic growth.

In summary, the last decade has witnessed substantial changes in both the RBI and the Indian government. These reforms have stabilized inflation, improved banking health, and reduced volatility—issues that once hindered foreign investment and domestic growth. The RBI’s growing credibility has strengthened its ability to influence economic growth through monetary policy and the rupee, while also enhancing its capacity to shape the banking industry.

Structural Contradictions: A Savings Glut?

While India has made strides in achieving macroeconomic stability, structural contradictions persist. One of the key issues is the “savings glut” that has emerged, particularly in the wake of the COVID-19 pandemic. This has led to a K-shaped recovery, where wealthier segments of society—especially those invested in the stock market and luxury goods—have seen significant gains, while lower-income workers, especially those in the informal sector, have faced stagnant wages.

The informal sector has been hit particularly hard by several factors. Speculation in asset prices, driven by low corporate taxes and capital gains taxes, has indirectly harmed these workers. Policies such as demonetization, the introduction of the GST, and the lockdowns have disproportionately affected the lower class, exacerbating the inequalities already present in the economy.

There has also been a rise in NPAs due to shadow banking, which is largely financed by high-net-worth individuals engaging in speculative lending. The result has been riskier loans and inflated real estate prices, driven by excess liquidity rather than productive investment. Affordable housing, for example, which was growing rapidly before the pandemic, has been crowded out by speculative activity in real estate. Additionally, low-income groups are increasingly relying on unsecured credit, such as buy-now, pay-later schemes, which has led to higher default rates.

These trends have had political implications as well. In 2024, four years after the onset of the pandemic, Prime Minister Modi suffered significant losses in certain areas, particularly in education, wages, and issues facing the lower class. Dr. Acharya’s analysis of the savings glut helps explain this, with growing inequality fueling discontent. For example, the stock market's growth has largely benefited retail traders, but only about 5 percent of the population can invest. Meanwhile, policies such as taxation and stringent lockdowns have hurt lower-income groups, leading to a $12 billion (₹1.1 trillion) tax cut being announced to address some of these issues.

Dr. Acharya’s Policy Recommendations

To address these structural challenges, Dr. Acharya has proposed several policy recommendations. First, he advocates for reducing tariffs, in line with the US government's stance, to encourage foreign direct investment (FDI) in sectors such as technology and manufacturing. This would help India reduce its reliance on China and foster growth in these critical industries.

Another key recommendation is to break up the large conglomerates that dominate India’s business landscape, such as Adani, Ambani, and JSW. By de-conglomerating these massive firms, Dr. Acharya believes India can promote the growth of mid-sized companies and increase competition. The majority of Indians still work for small-to-medium-sized enterprises (SMEs), which are being squeezed out by the dominance of oligopolies. More competition would improve innovation and, in turn, raise worker living standards.

In terms of fiscal policy, Dr. Acharya calls for higher taxes on the wealthy, particularly by increasing capital gains taxes to reduce financial speculation in the equity markets. He also advocates for removing unnecessary corporate subsidies that lead to rent-seeking behavior, where companies profit off of government support without providing significant utility. The new tax plan already incorporates his third recommendation: redistributing demand from the rich to the poor.

On the monetary front, Dr. Acharya suggests narrowing the target for core inflation to 4 percent, rather than maintaining a wider band. While emerging markets can tolerate higher inflation due to rapid growth, the post-COVID inflation has disproportionately eroded purchasing power for poorer consumers. Welfare and agricultural subsidies, which form the backbone of India’s economy, must also be reformed. For instance, fertilizer subsidies, valued at $21 billion (₹1.8 trillion), have been criticized for degrading soil and groundwater without providing measurable benefits.

In conclusion, Dr. Acharya’s insights into India’s macroeconomic stability and the structural challenges it faces provide a nuanced understanding of the country’s economic trajectory. His policy recommendations offer a roadmap for addressing inequality, fostering competition, and ensuring sustainable growth in the years to come.

Message from our Sponsor

Hands Down Some Of The Best 0% Interest Credit Cards

Pay no interest until nearly 2027 with some of the best hand-picked credit cards this year. They are perfect for anyone looking to pay down their debt, and not add to it!

Click here to see what all of the hype is about.

Gupshup.

Macro

India's wholesale inflation stayed steady at 2.31 percent, lower than the 2.5 percent predicted by economists, as food and fuel prices moderated. Vegetable inflation saw a sharp decline, while cereal and manufactured goods prices continued to rise.

Equities

Glenmark Pharmaceuticals missed profit estimates for the third quarter as weak U.S. demand for its chronic illness drugs offset strong India sales. While net profit rose to 3.48 billion rupees, it fell short of expectations amid pricing pressures and sluggish growth in North America.

Hexaware Technologies’ $1 billion (₹87.5 billion) IPO was fully subscribed in the final hours, driven primarily by institutional buyers as retail demand remained weak amid a broader market downturn. The IT exporter, backed by Carlyle, is aiming for a nearly $5 billion (₹437.5 billion) valuation, despite market volatility and investor caution over high-priced IPOs.

Asian Paints is exiting Indonesia by selling its business to Australia’s Omega Property Investments for $5.6 million (₹490 million), citing growth challenges after nine years in the market. The move will result in a $10.4 million (₹910 million) loss for the company, which derives most of its revenue from India.

GlaxoSmithKline Pharmaceuticals India reported a 35 percent rise in adjusted profit for the third quarter, driven by strong demand for respiratory drugs and its antibiotic Augmentin. The company’s revenue grew 18 percent, aided by the success of products like Shingrix, despite pricing constraints on some medicines.

Google's head of public policy in India, Sreenivasa Reddy, has resigned, marking the second departure in this critical role in just two years. The company is now appointing Iarla Flynn as the interim policy lead for India, a key market for Google amidst ongoing regulatory challenges.

Alts

India is expected to invite bids this year for 114 multi-role fighter jets, a long-delayed effort to modernize its aging air force amid growing competition from China and Pakistan. Major global defense firms, including Lockheed Martin, Boeing, Dassault, and Saab, are positioning themselves for the contract, with an emphasis on local manufacturing partnerships.

Music labels across India are joining a class-action copyright lawsuit against OpenAI. Sony, Zee, and other large labels plan on suing OpenAI together, further complicating the LLM’s legal struggles in India. Although the country is its 2nd largest user base, it keeps facing allegations of borrowing or stealing content though the company alleges all material is under fair use.

Adani-backed firm is among three finalists for taking over production of India's small satellite launches. ISRO is turning SSLVs into a private matter to expand India’s commercial space sector — especially for low earth orbit (LEO) which is the most sought-after space real estate currently. The winning company of the finalists will have to pay $30 million (₹3 billion) in initial rights with figures after the first two years still unknown.

India has increased the budget for its Gaganyaan human spaceflight mission to $2.32 billion (₹201.1 billion), expanding the project to include a national space station and planning multiple crewed and uncrewed missions by 2028. The mission aims to send Indian astronauts into space and safely return them, a milestone previously achieved only by the U.S., Russia, and China.

Adani Power will fully restore electricity supply from its 1,600 MW Indian plant to Bangladesh within days after a three-month reduction due to payment delays, but it has refused Dhaka’s requests for discounts and tax concessions. While the resumed supply meets Bangladesh’s rising summer demand, negotiations continue over financial terms, with Adani insisting on strict adherence to the power purchase agreement.

Coinbase is working on returning to the Indian market after halting operations over a year ago, engaging with local authorities to secure approvals. The company expressed excitement about India's potential, while the country reviewed its cryptocurrency regulations amid global shifts.

Policy

India's new income tax bill grants authorities sweeping powers to access taxpayers' emails, trading accounts, and social media during searches, with the ability to override systems if access is denied. The bill, which aims to modernize the 1961 tax law, covers digital spaces such as cloud and banking accounts, raising concerns about privacy and potential misuse.

India has cut tariffs on bourbon whisky from 150 percent to 100 percent, a move benefiting U.S. brands like Jim Beam, following criticism from President Trump over trade barriers. The reduction, seen as a gesture to ease tensions and avoid retaliatory tariffs, signals India’s willingness to adjust duties for key trade partners

The U.S. has approved the extradition of Tahawwur Rana, a suspect in the 2008 Mumbai attacks that killed 166 people, President Donald Trump announced alongside Indian Prime Minister Narendra Modi. Rana, a Pakistani-origin businessman, will be sent to India to face charges for his alleged role in the attacks.

See you Monday.

Written by Yash Tibrewal. Edited by Shreyas Sinha.

Disclaimer: This is not financial advice or recommendation for any investment. The Content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice.