In partnership with

Good afternoon,

Welcome to the best way to stay up-to-date on India’s financial markets. Today, we’re discussing

Indian banks want more flexibility with cash reserve requirements,

the RBI believes India can withstand broader global volatility,

Nifty Bank index surges over $100 billion despite weak fundamentals.

Then, we close with Gupshup, a round-up of the most important headlines.

Have a question you want us to answer? Fill out this form and you could be featured in our newsletter.

—Shreyas, [email protected]

Market Update.

Banks Urge the RBI to Ease Daily Cash Norms.

Indian banks have requested the RBI to provide more flexibility in maintaining their daily cash reserve requirements, according to people familiar with the discussions. A decline in cash requirements would allow more cash to be used as loans, which could stem declining credit in India. This comes as the central bank considers overhauling its liquidity management framework in response to rapid shifts in the digital banking landscape, something that has already opened the taps in regard to consumer credit.

Banks seek lower daily CRR mandate: Currently, banks are mandated to maintain a Cash Reserve Ratio (CRR) of 4 percent of their total deposits, calculated and reported on a fortnightly basis. Of this, 90 percent must be maintained daily, ensuring adequate liquidity at all times. The US has no reserve requirement but has capital requirements of 4.5%. The key difference is that a capital requirement is not mandated to be liquid assets.

In a recent meeting with senior RBI officials, the second such interaction in recent weeks, bankers proposed reducing the daily maintenance requirement to 80-85 percent, offering them greater operational flexibility while still adhering to overall CRR norms. Part of the greater flexibility is from reducing dependence on the RBI or 3rd party repo facilities. Currently, banks have to utilize repo lending to ensure there are ample reserves on hand; the RBI only conducts fortnightly repo facilities if it deems necessary, which can make reserve borrowing outside of that time period far more costly.

The request highlights growing concerns among lenders about managing liquidity in a banking system that now operates on a 24/7 digital payments infrastructure, where real-time fund transfers can lead to sudden, large withdrawals even outside traditional banking hours.

Liquidity management challenges: The RBI has been reviewing its liquidity framework, especially in light of findings from a recent internal panel report. The report underscored the need for banks to hold sufficient overnight liquidity buffers to deal with unexpected outflows, particularly after money markets shut for the day. The RBI has not yet publicly responded to the bankers’ request, and an email sent to its spokesperson had not been answered at the time of publication.

More suggestions from the banking sector: In addition to the CRR adjustment, banks urged the central bank to continue with its daily variable rate reverse repo operations — a tool for short-term cash infusions. While the RBI traditionally relies on the 14-day repo for liquidity management, it has recently skipped these auctions, prompting concerns among lenders. Bankers also floated the idea of fixed-rate loans tied to a percentage of their deposits, which they believe would help better manage liquidity in an increasingly volatile environment. Those fixed loans would have less variable rates, something that has become more prevalent globally since rapid central bank and trade decisions have impacted short-term rates.

Discussions also touched on the operating rate of the monetary policy, currently anchored by the weighted average call rate (WACR) — an unsecured interbank lending rate (an uncollateralized loan between banks, making it more risky than a secured rate). Opinions were divided on whether to maintain the WACR or shift to a secured rate for greater stability and predictability. The conversation reflects broader questions about how India’s monetary policy transmission can adapt to structural changes in financial markets and banking practices.

Indian Economy Resilient Amid Global Headwinds, Says RBI.

The RBI expressed confidence in the Indian economy’s ability to withstand global uncertainties, citing robust domestic demand and a supportive environment from government spending, plus the RBI's accommodative stance. In its latest State of the Economy report released on Wednesday, the central bank emphasized a cautiously optimistic outlook for the fiscal year, despite ongoing global trade disruptions and geopolitical tensions.

The RBI stated that India is well-positioned to navigate global headwinds, attributing this resilience to strong domestic consumption, government-led capital expenditure, and the buoyant services sector. While the global economy remains fraught with uncertainty, particularly due to trade frictions, the RBI maintained its growth projection of 6.5 percent for FY25.

This is in contrast to more conservative forecasts from international financial institutions. Morgan Stanley and Goldman Sachs, for instance, recently lowered their growth estimates to 6.1 percent, citing the adverse effects of trade tensions and weak global demand.

Domestic tailwinds supporting growth: The central bank highlighted easing inflation, healthy rainfall forecasts, and a strong rabi (winter) harvest as key tailwinds supporting the Indian economy. These factors are expected to boost rural demand and keep food inflation under control, reinforcing overall macroeconomic stability.

The RBI noted that an above-normal monsoon, as forecast by the weather department, would likely aid agricultural output and rural income, further supporting consumption-led growth in the coming quarters.

Cautious optimism: While acknowledging external risks, the RBI’s tone remains optimistic. The report underscored the importance of policy support, resilient domestic demand, and ongoing structural reforms. As India moves deeper into FY25, the central bank’s confidence provides reassurance amid global economic volatility. However, it remains to be seen how prolonged trade disruptions and geopolitical developments will ultimately shape the economic trajectory.

The Banking Sector’s Rapid Rise and Risk.

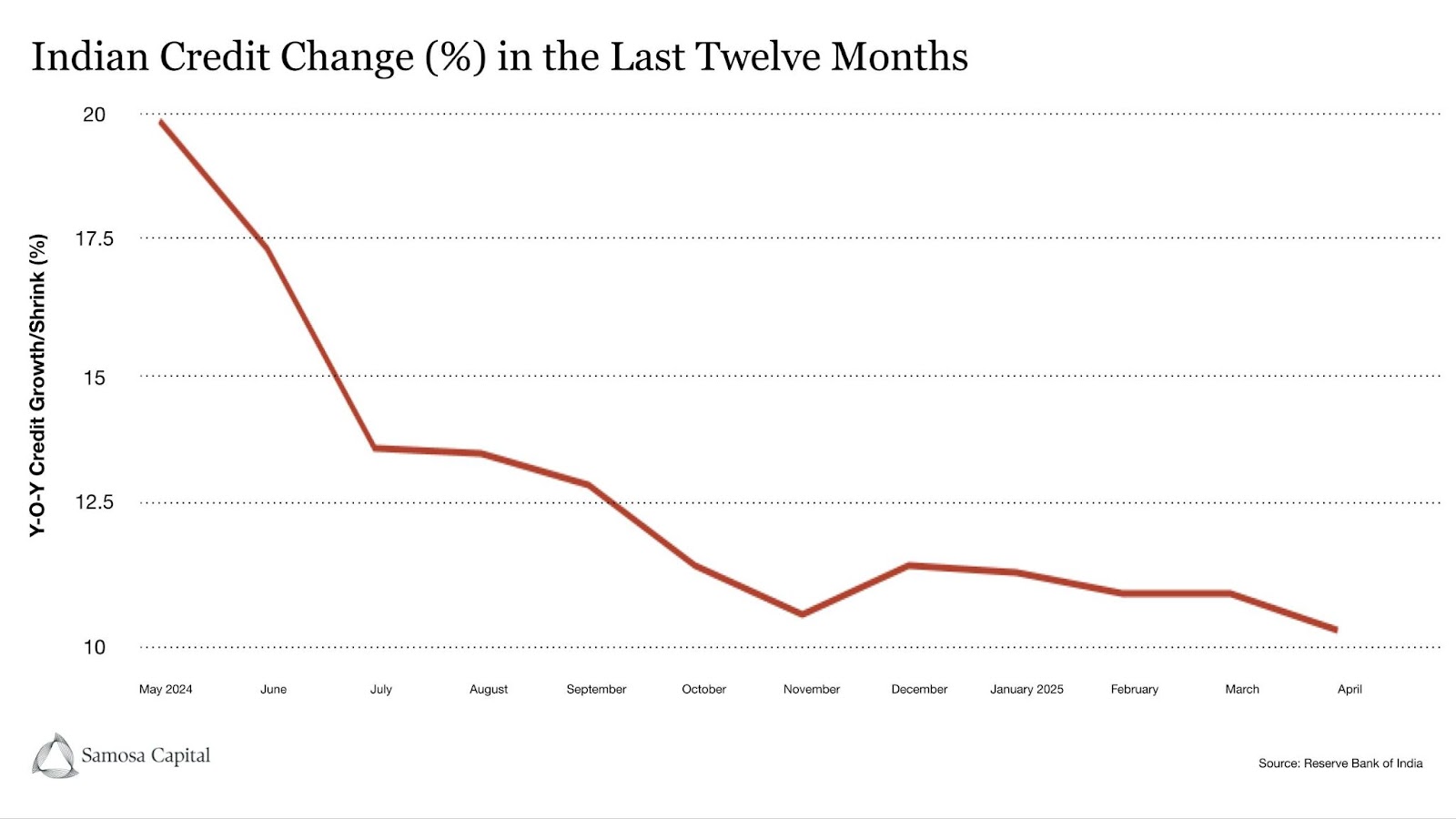

Over the past month, the Nifty Bank index has surged over $100 billion (₹8.6 trillion), driven by hopes of RBI rate cuts and regulatory support. But this rally follows a period of sluggish fundamentals.

Annual credit growth has slowed from 16 percent in 2021 to around 11 percent. Corporate demand — nearly half of all loans — remains weak, while retail and unsecured lending haven’t rebounded amid tepid urban consumption. SME lending is growing, but from a low base and remains vulnerable to shocks like Trump-era tariffs. Consumer debt is increasingly unsecured, and demand is still soft.

Recent foreign interest highlights structural issues. After a $1.2 billion bailout of Yes Bank by Indian lenders, Japan’s SMBC bought a 20 percent stake — the largest such investment in a decade. But this shows less about Yes’s strength and more about the RBI’s last-resort openness to foreign capital, as seen before with Fairfax (Catholic Syrian Bank, 2016) and DBS (Lakshmi Vilas, 2020).

Meanwhile, Emirates NBD is moving toward becoming a full Indian subsidiary, possibly to buy IDBI Bank. Despite optimism about foreign competition, the RBI remains selective. True benefits like lower rates and more choice haven’t materialized, with five major banks still dominating.

At IndusInd, once praised for micro-lending, a widening accounting shortfall — possibly deliberate — raises governance concerns. While isolated compared to the past NPA crisis, it’s a reminder that strong balance sheets (NPAs at 2.4 percent, capital adequacy at 16 percent) don’t eliminate the need for vigilance. Without faster GDP growth, these buffers may sit idle as revenue momentum fades.

Message from our sponsor.

The 5 Advantages of a Gold IRA

With everything going on in the world today - inflation, tariffs, market volatility - it’s more important than ever to stay informed.

That’s why you need to get all the facts when it comes to protecting your retirement savings.

Did you know that Gold IRAs can help safeguard your money?

Request a free digital copy of The Beginner’s Guide To Gold IRAs to arm you with the facts.

In the Beginner’s Guide to Gold IRAs, you’ll get…

The Top 5 Advantages to a Gold IRA

How To Move Your 401K To Gold Penalty Free

A Simple Checklist For How to Get Started

Don’t miss this opportunity to get the facts about how a Gold IRA can help you protect and diversify your retirement savings.

*Offer valid on qualified orders of Goldco premium products only. Receive up to 10% in free silver based on purchase amount; cannot be combined with other offers. Additional terms apply—see your customer agreement or contact your representative for details.

Reach out to [email protected] to sponsor the next newsletter!

Gupshup.

Macro

Credit growth continues to slow from 16 to 11 percent. Demand for loans has weakened across the economy, from big businesses to nonrecourse consumers. At the same time, balance sheet health is arguably the best it's ever been, and delinquencies across microfinance and consumers are low.

Flash PMIs show economic activity is high at 61.2. Composite was up to 59.7 in April; manufacturing was at 58.3 (mostly flat m-o-m), and services rose 2.5 points to 61.2. Business confidence is very high right now, with firm pickups in demand and employment, even with geopolitical conflict and trade negotiations.

Short tenor bonds have rallied on RBI dividend expectations. The yield curve as a whole is bull-steepening (short-term rates are falling faster than long-term ones, causing a steeper upward slope).

Equities

Proxy firms recommend that IDFC Bank veto Warburg Pincus and the Abu Dhabi Investment Authority's board offer. It would involve a $877 million (₹75 billion) investment but also board seats for the two investors. Proxy firms have argued against board seats since there is no minimum shareholding threshold, and recent NPAs have been idiosyncratic rather than industry-wide, something that is easier to combat.

ONGC missed estimates with a net income decline of 35 percent. Profits fell to $753 million (₹64.5 billion) after ramping up investments in refineries, petrochemicals, LNG, and renewable assets. The R&D is growing its overall footprint from just being an oil explorer.

Consumer retail stocks still face cost headwinds. Urban general consumption is still under pressure as well, according to various distributors and dealers in major cities. Food categories are gaining more spending than general home and personal care, however.

Midcap companies vastly outperformed the Nifty 50 on earnings. Earnings growth for midcaps was 21.4 percent y-o-y compared to 4.3 percent for the Nifty. Demand growth and cost reduction impact smaller firms due to smaller product offerings. Smaller companies also have fewer cost hedging schemes, which can make deflation more impactful to margins.

Alts

IndusInd Bank owners, the Hindujas, pledge support after losses and suspected fraud. If more equity is needed, the chairman, Ashok Hinduja, said the family would pledge capital after the $262 million (₹22.4 billion) loss. The piling losses related to microfinance loans are being written as fee income, which has since been reversed.

Birla's Grasim Industries gets $117 million (₹10 billion), 5-year bond at 6.56 percent. This is its lowest-yielding local currency bond in 5 years, and the sole arranger was Axis Bank. Grasim is a leading textiles and chemicals producer.

Adani Ports raised a $150 million (₹12.8 billion) loan from DBS at 5.5 percent for Capex spending. The loan is denominated in dollars as a 4-year facility, with this being the first bilateral loan from a global bank since the US indictment.

Bajaj Auto is using a $907 million (₹77.5 billion) debt package to buy the minority stake of KTM AG. Bajaj already has an interest in the Austrian bike company, but would take sole control. KTM is under bankruptcy proceedings, and the cash would allow it to pay off creditors. This would give Bajaj more entry into the global bike market.

Policy

Modi ruled out talks with Islamabad and vowed to make Pakistan pay for any infractions. He said that any more militant or terrorist activity would lead to Pakistan paying with its army and economy. No trade will resume as both countries make pleas to the international community to raise support.

India says a top Maoist rebel was killed in a raid against extremists. Home Affairs Minister Amit Shah said that 27 rebels, including the leader, were killed. Maoist rebels oppose parliamentary democracy and are spread across the mineral-rich central and eastern regions.

See you Friday.

Written by Yash Tibrewal. Edited by Shreyas Sinha.

Disclaimer: This is not financial advice or recommendation for any investment. The Content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice.