Hello. We need your feedback to make this newsletter more useful to people like you. Please let us know what you think here.

Anyways… just hours after last week’s Samosa Capital newsletter hit your inbox, results from the Indian election started trickling in and Modi was delivered a far larger upset than expected. Markets fell dramatically after an exceptionally strong rally on the false flag that Modi’s BJP would be able to maintain a single-party majority. Awkward.

We’ll go through three reasons why we (and everyone else) got it wrong, talk about a disconnect in attitudes toward Indian markets by foreign and local investors, and then finish with a round-up of the most important headlines from the week.

BTW: In the United States, around 60 percent pay income tax. What percent of Indians pay income tax? Answer at the bottom — I bet the answer will surprise you.

Markets

Equities | Last Close | 1 Week | YTD |

|---|---|---|---|

NFTY | 278.51 | -0.02% | 6.98% |

FLIN | 38.99 | -1.24% | 11.88% |

MSCI EM | 1073.14 | 0.36% | 5.58% |

SP500 | 5360.79 | 1.46% | 13.03% |

MSCI India | 54.15 | -1.19% | 11.26% |

Other | Last Close | 1 Week | YTD |

|---|---|---|---|

USDINR | 83.514 | 0.51% | 0.37% |

EURINR | 89.911 | -0.78% | -2.42% |

Gold | 2311.1 | -1.48% | 11.46% |

Coal (Spot) | 131.45 | -7.69% | -0.34% |

Indian 10YR | 7.018 | 3.20bps | -16.00bps |

U.S. 10YR | 4.434 | -6.80bps | 49.80bps |

Quick Appendix: NFTY is a weighted average of the largest 50 companies listed in the National Stock Exchange of India by market capitalization. FLIN, or Franklin TSE India ETF, tracks large and mid-cap companies, weighted by market cap, to give international investors exposure to Indian markets. MSCI EM is an index that captures large and mid-cap companies across 24 emerging market countries and covers 85% of the free float-adjusted market capitalization in each country. SP500 is the index of the 500 largest companies listed in U.S. stock exchanges by market cap. MSCI India is an index that covers 85% of the Indian equity universe. Data as of close of market Friday in India.

Modi’s Election Setback: 3 Reasons Why Everyone (Including Us) Got it Wrong

Last Monday, we reported that markets, currencies, and bonds had experienced a strong upward rally thanks to exit polls showing a strong showing for BJP after election polls had closed. Within hours of the vote counting beginning, Prime Minister Modi’s party, the BJP, began facing unexpected setbacks, causing the Nifty50 index to close down 5.93 percent at end of day, and experience its worst intraday decline since March 2020.

Results:

Modi’s BJP won 240 seats, far short of the 303 it won in the 2019 election, and less than the 272 seats needed to keep a single-party majority.

Modi will rely heavily on the National Democratic Alliance (NDA), a right-of-center coalition composed of the BJP and smaller parties, in order to maintain power.

BJP’s national vote share only declined by 0.7%, from 37.3% in 2019 to 36.6%, and actually won an extra 6.90 million votes in 2024 compared to the previous national election. This small decline in vote share cost the BJP 63 seats in Parliament, as the party tends to win seats by large margins but lose them by very narrow ones.

India’s first-to-the-post system allows candidates to win a seat without a majority as long as they collect more votes than their opponents

The Indian National Democratic Inclusive Alliance (INDIA), which is the opposing coalition to the NDA and led by the Indian National Congress party, won 234 seats

Reason 1: Polling

Last week, we noted that, given a decade-long trend of Indian polls undercounting BJP support, exit polls predicting a strong win for Modi were likely accurate, if not conservative. For the first time, the opposite was true.

Discrepancies in exit polling, which also caused wrong predictions in the U.S. 2016 presidential election, often arise from “secret supporters”—voters who back candidates like Modi in India or Trump in the U.S. but falsely claim to pollsters that they voted for the opposition.

Reason 2: Uttar Pradesh

The northern state home to the Taj Mahal is the country’s most populous and has been a stronghold of BJP support. In 2014, the BJP won most of the seats, 62 of 80. Last week, it was only able to secure 33, with most flipping to Samajwadi Party, a local socialist political group part of the INDIA coalition.

This is especially troubling considering Modi himself if a member of parliament representing a constituency in Uttar Pradesh, a strategic political move Modi made despite hailing from and previously leading the state of Gujarat.

Earlier this year, Modi inaugurated a temple in Ayodhya, a city in Uttar Pradesh considered to be the ancient birthplace of the Hindu god Ram. Considered an auspicious and highly supportive event for his supporters, many have interpreted the BJP’s loss in the state as the voters saying economic progress is far more important than Hindutva (pro-Hindu) policies.

Considered an auspicious and highly popular event by his supporters, many interpret the BJP's loss in the state as voters reminding leadership that economic progress still trumps Hindutva (pro-Hindu) policies in importance.

Reason 3: Unemployment

India still has hundreds of millions depending on welfare for survival and is still recovering from a sharp decline in middle-income earners (many who were forced back into poverty) during the COVID-19 pandemic. The economic recovery paired with high inflation means that India’s middle class likely did not benefit from India’s strong GDP growth as much as lawmakers had hoped. Among its economic pains, structural unemployment stands out as a difficult one for India to solve; we wrote the below on India’s unemployment crisis two weeks ago:

This is largely driven by what experts call a decade of “jobless growth.” In an interview with Fareed Zakaria GPS, former RBI chair Raghuram Rajan said that India’s economy is driven by a “population dividend.” India’s GDP growth, which still lags behind other countries’ peaks like China, Taiwan, and South Korea at 10%, is far more attributable to a fast-growing population than it is to wealth creation. India’s GDP per capita has grown more slowly than Thailand, Indonesia, or Bangladesh since 1970.

Another telling sign of India’s employment crisis is that low-paying civil service jobs (called “peons”), which require no more than an elementary school education, often receive millions of applications from those far too qualified. When the northern Indian state Uttar Pradesh posted a job for 368 peon jobs; 2.3 million applied, including thousands of PhD holders. In another case, hundreds of doctors and lawyers were interviewed for a peon job in the northwestern Indian state of Rajasthan.

Foreign and Domestic Investors See Two Different Indias

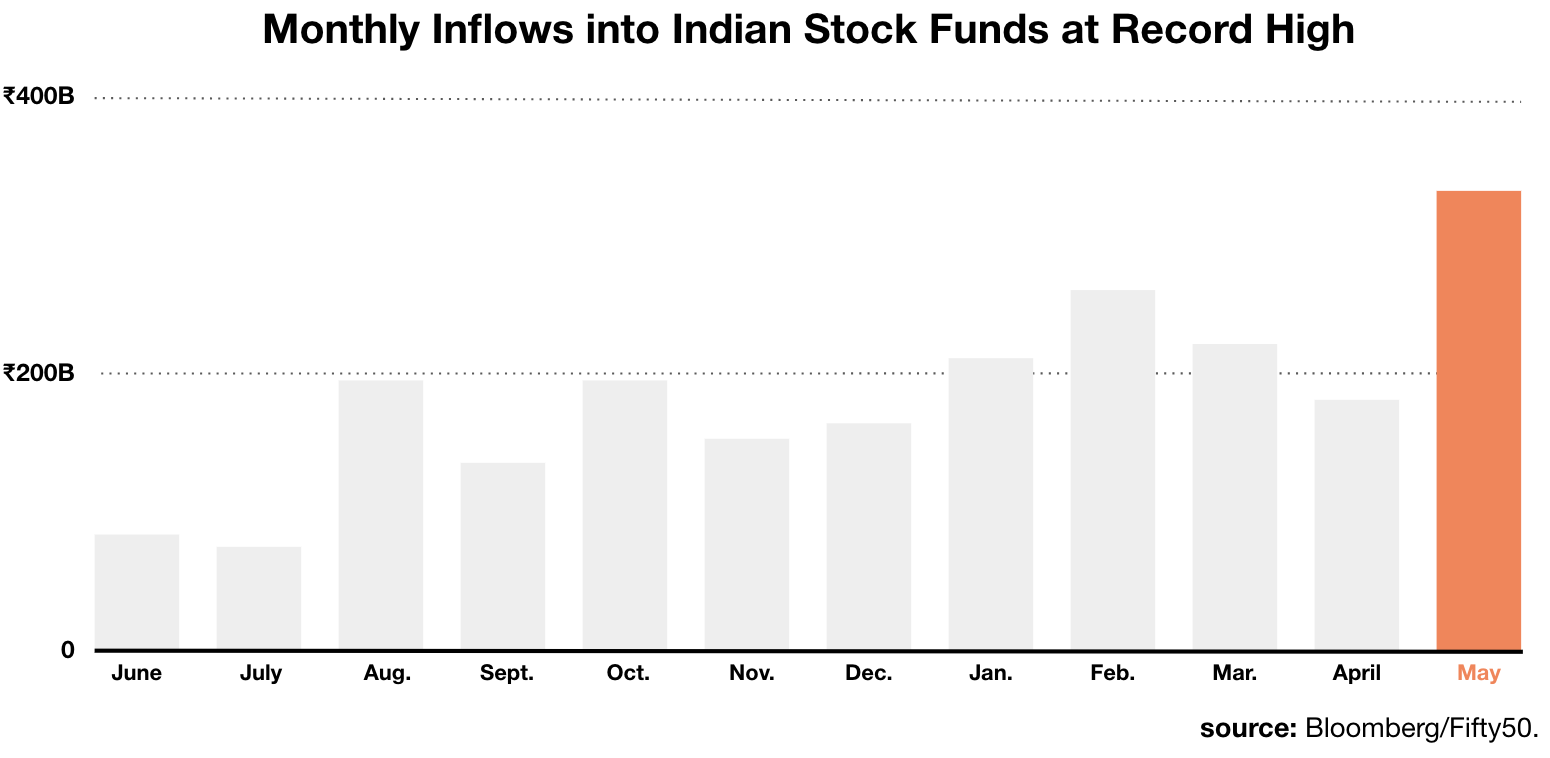

May closed with $4.2 billion (₹347 billion) of inflows into equity mutual funds, the fastest rise on record. Driven by local retail investors who see higher return opportunities in equities than government notes and bonds, inflows occurred despite volatility from the ongoing elections. May is the 39th month consecutively that Indian equity mutual funds have received net positive inflows.

However, past the Indian Ocean are different narratives of the country’s future. Foreign investors are pulling money out of India, and Asia overall, in droves: $3.06 billion in foreign money exited Indian markets in May, the highest outflow of any Asian country. It is the second month in a row Indian markets have experienced outflows. Kunal Vora, BNP Paribas’ head of India equity research told Reuters that international investors are waiting for the dust to settle in Indian politics. As the Modi administration forms government and reinstates familiar policymakers, investors might feel more confident in reinvesting in India.

There are two primary reasons for the disconnect between retail and foreign investors:

U.S. Dollar Strengthening: Strong economic data from the U.S., along with CPI prints higher than the 2 percent target, gives investors increased confidence that the Federal Reserve will delay rate cuts. This, alongside weak economic data and snap elections in Europe, strengthens the U.S. dollar and makes returns in U.S. markets more attractive, while money stored abroad immediately becomes less valuable to Western investors. Emerging market equities automatically suffer as a consequence

An Indian Revolution: With Indian mutual funds seeing 39 consecutive months of inflows, retail investors are showing consistent optimism that weathers any short-term volatility that spooks international money. And there’s a good reason: The Nifty50 often hits record highs, as it did after Modi’s election last week, and has consistently grown in the last four years. Now, Indians have shown they are moving beyond the usual appetite for low-risk assets such as gold. Investment in equities is growing rapidly; the percent of wealth invested in equities by Indians doubled from 2013 to 2023. This overwhelming bullish attitude is also paired with an unusual risk tolerance: 78 percent of all option contracts globally were executed in India.

Equity analysts in India and abroad have upgraded their expectations for the Indian market to close at an all-time high by the end of 2024, Reuters reported in May.

Macro

Current account deficit continues to rise with 4.4% YoY growth in September Quarter (BusinessLine)

Current account deficit is caused when a country imports more goods and capital than it exports

The Economic Survey of 2022-23 cited rising commodity prices (with India being an importer of fuel and other essentials) and a weakening rupee making imports more expensive

Deficit grew 2.2% since April - June quarter

Emerging markets with current account deficits require foreign capital to finance the gap, which can become costly as India experiences two months of foreign investment outflows

India’s RBI keeps rates at 6.5% citing food inflation (FT)

This was widely expected as inflation continues to cascade to the 4% target

Indian households will experience increased food inflation over the next three months (BBG)

FY24’s GDP projection was raised from 7 to 7.2%

Rupee becomes favorite for carry investors, according to BofA (BBG)

Investors say the currency is cheap and low risk of depreciation, making it a favorite among EM currencies for carry investors

Long rupee is the only carry trade with positive returns among Asian currencies against U.S. dollar in 2024 thus far

Equities

Macro risks could lead to SBI’s valuations being slashed (Economic Times)

Most analysts still keep a buy target at 1,050 (₹12.65) but risk relapse or credit worries could occur

State Bank of India is one of the largest in India, but relies heavily on the public spending

Mukesh Ambani and Sunil Mittal take on Elon Musk for the Indian space race (FT)

Musk’s Starlink (the satellite internet service) has been trying to enter India since 2021, off of a positive relationship between Musk and Modi

Bharti Airtel and Reliance’s Jio are attempting to gain approval to launch satellites, but Starlink is reportedly ahead in the process, and its 6,000 existing satellite network

Retail traders push Indian option volume higher than SP500 - amid the meme stock rally (FT)

Notional value of Indian options traded per day is now $1.64T compared to $1.44T in the US

This rise has been driven by 0DTE options (options expiring within a week) due to volatile price moves

Alts

SMID credit growth likely to rise in 2H24 (BusinessLine)

The Economic Survey presented to Parliament revealed that credit growth in SMIDs (small and mid-cap companies) should rise as economic uncertainty fades

SMIDs experienced a 31% growth in credit issuance in FY22

VCs make up 85% of total impact investing in India (FT)

Climate tech, microfinance (availability of financial tools to all), and agrifood are starting to see greater inflows

Low startup costs and scaled-down bureaucracy make India a thriving environment for impact investing

Generalist VC funds earn an average IRR of 20-25% in India currently

EM Traders increase local debt investment as global carry trades unwind (BBG)

A rising dollar is causing carry trades (borrowing one currency to fund others) unprofitable

Investors are now finding greater opportunities in sovereign and corporate EM debt

PE’s growing dry powder stockpile is creating chances in APAC region (BBG)

IRRs in India frequently range between 20-25%

Growing funds and reallocation of capital is leading to greater investment in India

Politics

Nirmala Sitharaman Re-Appointed to Finance Minister Role (BBG)

Modi has decided to keep most of his cabinet during his third term as Prime Minister

Sitharaman has been lauded as a sensible and pragmatic finance minister by international investors

Adani stocks fall 20% on the back of Modi’s surprising election downturn (FT)

Two flagships - Adani Enterprises and Adani Ports - were down over 20% with negative news surrounding Modi’s performance

There was a wide market sell-off in public infrastructure-related stocks

Most analysts believe that premiums associated with public companies are being slashed, though this drawdown is extreme

India’s rosy 8% FY growth is misleading considering public spending and economic reporting (WSJ)

While FY23 featured a stunning 8% growth, companies continue to not spend even with tax cuts and private spending only accounting for 4% of growth

India’s calculations (using a small subset of firms to estimate all small businesses, price adjusting for GDP, unemployment, etc.) create better than actual numbers

Modi forced to rely on two major partnerships to form a coalition to take majority seats in parliament: Telegu Desam Party and Janata Dal-United (NYT)

Both parties frequently shift alliances; are far more moderate and secular; and have seen leaders’ names Naidu and Kumar come up for prime minister elections

We need your feedback to make this newsletter more useful to people like you. Please let us know what you think here.

And, consider sharing with three friends.

Oh, and only 1-2% of Indian adults pay any income tax at all. This is exceptionally low for a major economy. Income tax and the GST (India’s version of the VAT or sales tax) make up 90 percent of India’s tax revenue.

See you next week.

Disclaimer: This is not financial advice or recommendation for any investment. The Content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice.

1 USD = 83.57 Indian Rupee